A low credit score is a roadblock to achieving your financial goals. A poor credit score can hinder opportunities. It can also cost you more in the long run.

Consider the frustration of getting a loan or paying higher interest rates than you deserve. Each rejection or extra dollar spent on high fees can be a setback. It makes achieving the financial freedom you’ve been working toward harder. The worst part? Without the right strategies, improving your credit score can take years. It will leave you stuck in a cycle of missed opportunities.

But what if there were a faster, more innovative way to boost your credit score? Understand the factors that influence your score. Also, you can leverage tools like authorized user tradelines. These help you take control of your financial future. In this article, we’ll explore practical steps to rank your credit score higher. We will show you how partnering with trusted companies like Coast Tradelines can help you reach your credit goals faster.

What is a Credit Score?

A credit score is a three-digit number that shows an individual’s creditworthiness based on their credit history. Credit bureaus calculate the score using various factors. It is crucial for lenders when evaluating potential borrowers. Credit scores range from 300 to 850. Higher scores show a lower risk for lenders, while lower scores may suggest potential financial distress.

Key Factors Influencing Credit Scores

Understanding the breakdown of a credit score can help you manage and improve it. The primary components include:

Payment History (35%)

This is the most significant factor in determining your credit score. It shows whether you pay your bills on time. On-time payment of your current and past credit accounts is crucial to your score. Late payments of credit card balances or loans, defaults, and bankruptcies can harm your score.

Credit Utilization Ratio (30%)

Credit utilization rate measures the amount of available credit you’re using. To maintain a good score, keep your utilization below 30% of your total credit limit. High utilization might raise red flags for lenders.

Length of Credit History (15%)

A longer credit history can contribute positively to your score. It does this by giving lenders a track record of your borrowing behavior. This includes the age of your oldest account, your newest account, and the average age of all your credit accounts. Consistent management and timely payments over an extended period can build lenders’ trust in your creditworthiness.

Types of Credit (10%)

The variety of credit accounts you hold can also impact your score. Having a mix of revolving credit (credit cards) and installment loans (e.g. mortgages or auto loans) shows your ability to handle various types of credit. But, it’s essential to manage each account. The wrong credit mix can have negative effects on your score.

New Credit (10%)

When you apply for new credit, lenders will usually perform a hard inquiry that can temporarily decrease your score. But, if you manage these new accounts responsibly, they can eventually contribute positively to your score. Limiting the number of credit applications made within a short period is advisable. This helps avoid repeated inquiries, which can signal financial distress to lenders.

Understanding Scoring Models

Financial institutions use various credit scoring models to calculate credit scores. Two of the most popular scoring models are FICO and VantageScore. While the fundamental elements influencing credit scores are similar, each model may weigh them differently.

FICO® Model vs. VantageScore Model

Developed by the Fair Isaac Corporation, the FICO® score is the most well-known credit scoring model in the United States. It affects lending decisions for a significant part of the economy. FICO scores range from 300 to 850, with higher scores implying lower credit risk. The FICO model emphasizes:

- payment history,

- amounts owed,

- length of credit history,

- new credit, and

- types of credit used.

Its different weightings focus on responsible credit usage.

Meanwhile, the three major credit bureaus created the VantageScore. These credit reporting companies are Experian, TransUnion, and Equifax. VantageScore also scores from 300 to 850 but with a bit different method. For instance, VantageScore places a stronger emphasis on recent credit behavior. It checks your payment history from the last 24 months. This means that VantageScore reflects the latest improvements on your late payment record faster than the FICO.

How Credit Score Ranking Works

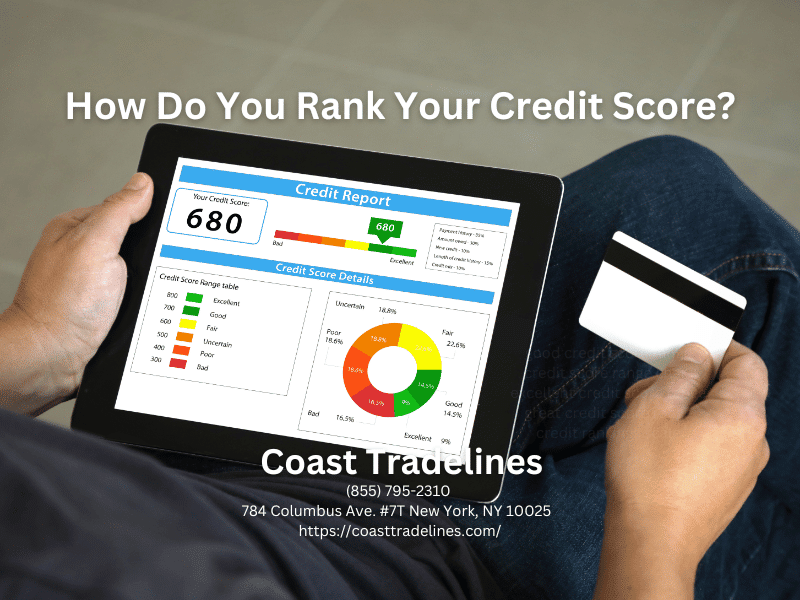

Scoring models categorize credit scores into different ranges. It allows both consumers and lenders to assess credit risk faster. Here’s a breakdown of how these models rank credit score ranges:

Excellent (760 and above)

Scores in this range show exceptional credit management. Exceptional credit scores pose minimal risk to lenders. Individuals with excellent credit scores will receive the best loan interest rates and terms.

Very Good (720 to 759)

This category reflects strong credit habits and a reliable repayment history. Borrowers with very good scores qualify for favorable loan conditions. They’re less competitive than those in the excellent range, though.

Good (660 to 719)

A good credit score suggests that you are responsible for managing your credit. People with good scores may face higher interest rates than those with very good or excellent scores. But they still have access to a variety of credit options.

Fair (580 to 659)

Those with a fair credit score may have a few credit challenges or missed payments. Lenders see them as a higher risk. It may result in higher interest rates and less favorable terms. Consumers in the average credit score range may need help securing loans or credit cards.

Poor (300 to 579)

Individuals with poor credit scores have a history of significant issues. This category indicates a high level of credit risk to lenders. Most often, it results in declined loans. You may also have very limited options with exorbitantly high interest rates. Those in this range may need to improve their credit profile to access better credit opportunities.

Financial Benefits of a Higher Credit Score

Having a higher credit score is not only a number. Your score represents a gateway to many financial benefits. It is key to a good credit journey and financial health. Here are some of the key advantages of maintaining a good or excellent credit score:

Lowest Interest Rates

One of the most immediate benefits of an exceptional score is access to lower interest rates financial products. Lenders feel more confident in offering you loans at competitive rates. This can lead to large savings over the life of a mortgage, auto loan, or personal loan.

Better Loan Terms

Beyond interest rates, a high credit score can translate into better loan terms. These could include larger loan amounts, reduced fees, or flexible payment terms. Financial institutions offer favorable terms like no annual fees on credit cards. They also provide extended payment periods on loans.

Increased Credit Access

With a strong credit score, you can access a broader range of financial services and products. This includes premium credit cards, lower fees, and extra perks. An excellent score means more straightforward loan applications.

Practical Aspects of Monitoring Your Credit Score

Regular monitoring of your consumer credit score is essential. It helps you understand where you stand in creditworthiness. Given its significant impact on your financial well-being, being proactive about your credit management is crucial. Here are some practical tips and strategies for efficient monitoring of your credit score.

Understand Your Credit Report

Familiarize yourself with your credit report. This document provides a comprehensive overview of your credit history. It includes details of your credit card accounts and loans. It also reflects any inquiries made by lenders. Review it for completeness and accuracy. Even a single error can have a negative impact on your score. You can get your annual credit report free from your chosen credit reporting agency.

Use Credit Monitoring Services

Consider enrolling in a credit monitoring service. This service can provide real-time updates on changes to your credit report. It is ideal for borrowers with credit scores below average. Many of these services track your score and alert you to irregular activities. Some services even offer identity theft protection. This allows you to safeguard your credit against fraudulent activities.

Establish Alerts and Notifications

Setting up alerts through your bank or credit card issuer can help you stay informed. Knowing crucial changes to your credit profile and financial activities is vital. You can customize these notifications depending on your preferences. By setting these alerts, you can keep track of your credit status. You can also take proactive measures to improve or maintain your score as needed.

Check Your Score Regularly

It’s prudent to check your credit score often. Many financial institutions and third-party services provide free access to your credit score. Aim to check your score at least once a year. It will help you understand how your financial habits are impacting your creditworthiness. Always checking your score allows you to identify and address any discrepancies or inaccuracies.

Improving Your Credit Score

Improving your credit score is essential for gaining access to better financial opportunities. Here are several strategies that can help elevate your credit score over time:

Build Credit Responsibly

Building credit is crucial for establishing a positive credit history. Begin with manageable credit accounts, such as secured credit cards or small loans. Make consistent, on-time payments without exceeding your credit limit. Over time, this responsible behavior will help you develop a healthier credit file.

Cut Credit Inquiries

Each time you apply for credit, your credit report makes a hard inquiry. While a few inquiries may not affect your score, only a few within a short period can signal risk to lenders. To avoid this, research your options before applying. Consider waiting until your credit score is desirable before seeking new credit.

Maintain On-Time Payments

One of the most critical factors in your credit score is your payment history. Always aim to make payments on time. Late or missed payments can drop your score. Consider setting up automatic payments or reminders if you need help remembering payment due dates. Also, if you cannot make a payment on time, it’s wise to contact your lender beforehand. Many companies may offer grace periods or deferment options. These options can help mitigate the impact of a late payment on your credit score.

Reduce Debt Utilization

Another significant factor in determining your credit status is your credit utilization ratio. You should aim to keep your utilization below 30%. Requesting a credit limit increase can also lower your utilization ratio. But, you must ensure you do not increase your spending.

Diversify Your Credit Mix

A well-rounded credit profile can also enhance your credit score. Credit scoring systems favor a mix of installment loans and revolving credit. But it’s crucial to manage these accounts. Only take on new debt when it’s prudent. Also, always focus on making payments in full and on time.

Be an Authorized User of a Credit Card Account

One effective way to boost your credit score is by becoming an authorized user on someone else’s credit card account. This strategy allows you to piggyback on another person’s established credit history. If you’re going in this direction, choose someone with a strong credit profile.

As an authorized user, the payment history associated with that credit card will appear on your credit report as if it were your own. Maintaining a good payment record can enhance your credit score if the primary user maintains a good payment record. That is why it’s crucial to pick someone responsible for their credit. Poor payment behavior from the primary cardholder can hurt your score.

Being an authorized user does not give you control over the account. You won’t be responsible for making payments or incurring debt. The primary account holder’s actions will affect yours. That is why it is crucial that both parties are on the same page.

The most ideal is to be an authorized user of someone you know. If it’s not workable, that is where tradeline companies come in. Tradeline companies like Coast Tradelines offer various tradeline options. In our company, we have seasoned tradelines to choose from. These tradelines are long-time credit card accounts with excellent credit and payment profiles.

Final Thoughts

Your credit score is a reflection of your financial health. Improving your credit score doesn’t have to take years. With the right strategies, you can see significant improvements in a short time.

One powerful tool for boosting your credit score quickly is authorized user tradelines. You can enjoy its positive credit history by becoming an authorized user on a seasoned credit account. This can enhance your credit profile by increasing your average account age and lowering your credit utilization ratio. Both of them are key factors in determining your score.

The effectiveness of tradelines depends on working with a reputable company. Trusted providers like Coast Tradelines offer verified high-quality tradelines. We ensure transparency, reliability, and compliance with industry standards. This gives you peace of mind while investing wisely in your financial future.

If you’re serious about improving your credit score, explore authorized user tradelines as part of your strategy. Don’t let a low credit score hold you back. Act now to build the credit you deserve!