Many people struggle with low credit scores, making securing loans or getting favorable interest rates difficult.

You might be paying higher interest rates on loans without a good credit score. You may also face denial for credit cards. This can feel frustrating, especially when you don’t know where to start to improve your credit profile.

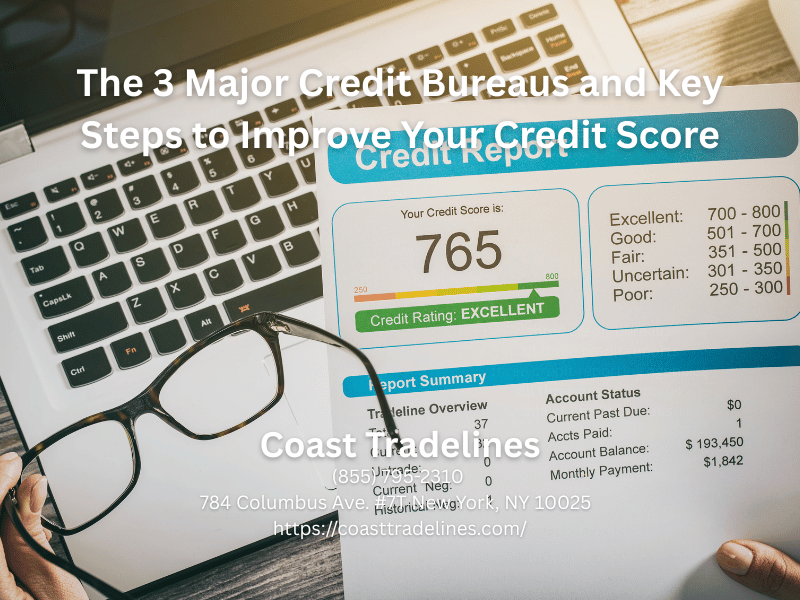

You can regain control of your financial future by understanding the three major credit bureaus and taking key steps to improve your credit score. With a few simple, strategic actions, you can see significant improvements in your creditworthiness. Let’s check into how these bureaus work. Look into the actionable steps you can take to boost your score.

What Are the 3 Major Credit Bureaus and Their Core Mission?

Equifax, Experian, and TransUnion are the three major nationwide credit bureaus. They play a pivotal role in the financial ecosystem. They collect and maintain consumers’ credit information. Each bureau gathers data related to individual credit histories. These information are crucial for constructing comprehensive credit reports.

Equifax

Founded over a century ago, Equifax operates in Atlanta, Georgia. The company serves millions of consumers and businesses around the globe. Its core mission is to provide insights and predictive analytics. Equifax also provides data protection and a suite of identity theft and fraud prevention services.

Experian

Experian is also entrenched in financial information services with its global operations in Dublin, Ireland. Known for its robust data security measures, Experian aims to empower consumers and businesses with the tools and insights. It provides services that range from credit reporting to assisting companies in fraud prevention and risk management.

TransUnion

TransUnion operates from Chicago, Illinois. Its mission is to help build trusted relationships between consumers and businesses. The company facilitates the smooth exchange of accurate and reliable information. The bureau provides an array of services. This includes credit reporting, fraud prevention, and credit score analysis.

How Credit Bureaus Impact Your Financial Life

The information managed by the credit bureaus plays a critical role in your financial profile. They’re crucial when applying for an auto loan, credit card, or mortgage. Your credit report is the primary tool lenders and banks use to assess your creditworthiness.

Credit Scores Explained

Each credit bureau generates a credit score using proprietary algorithms. These algorithms may differ. But the fundamental factors considered are similar across all three. Here’s a breakdown of what influences your credit score:

Payment History

This is the most significant component, accounting for approximately 35% of your score. It reflects your ability to make timely payments on all your debts.

Credit Utilization

This represents about 30% of your score. Credit utilization examines how much of your available credit you are currently using. Maintaining a low credit utilization ratio, below 30%, can boost your score.

Length of Credit History

This accounts for around 15% of your score. A longer credit history can boost your score. It helps paint a clearer picture of your credit behavior.

Types of Credit in Use

It makes up about 10% of your score. This aspect examines your various credit accounts, including revolving accounts and installment loans.

New Credit Inquiries

Also comprising 10% of your score, this factor considers recent credit applications. It also looks into how many new accounts you have.

How the Fair Credit Reporting Act (FCRA) Governs Their Operations

The Fair Credit Reporting Act (FCRA) is a pivotal piece of legislation. It governs the practices of credit bureaus in the United States. This ensures transparency, accuracy, and fairness in the reporting of consumer information. Here’s how the FCRA impacts the operations of the credit bureaus:

Accuracy and Accountability

Under the FCRA, credit bureaus must maintain the accuracy of the information in consumer credit reports. They must take reasonable steps to ensure that the data they collect and disseminate is correct and up-to-date. The bureau must investigate the dispute if a consumer identifies an error in their credit report. It should take place within 30 days.

Consumer Rights to Access

The FCRA provides consumers with the right to access their credit reports. You can access one from each major bureau free of charge once every 12 months. You may access it through AnnualCreditReport.com. This helps consumers stay informed about their credit status. It also helps them catch any inaccuracies early.

Disputing Errors

If the information is inaccurate, consumers have the right to dispute it. Upon receiving a dispute, a credit bureau must investigate. They must correct any determined errors. This process enhances the reliability of credit reports.

Your Credit Profile

Your credit profile reflects your financial behavior. It plays a significant role in determining your credit score. Lenders, banks, and other entities use it to assess your creditworthiness.

The Building Blocks of Your Credit File

Your credit report comprises several sections. These sections highlight your financial history and actions. These include:

Personal Information

This includes your name, address, and phone number. It also comprises your Social Security number and date of birth. This helps credit bureaus identify you and ensures the accuracy of your credit file.

Credit Accounts (Trade Lines)

This is information on your credit cards, mortgages, auto loans, and other types of credit accounts. Credit reporting agencies track your payment history, credit limits, and balances. They also check whether you’ve made payments on time.

Credit Inquiries

This refers to a record of when a business or an individual checks your credit report. These can be soft inquiries when you check your own credit. It can also be hard inquiries or when lenders check your credit for lending purposes.

Public Records

Public records include a history of bankruptcy, foreclosures, tax liens, or civil judgments. These serve as red flags for lenders and indicate potential financial distress.

Collection Accounts

It refers to any accounts sent to collection agencies due to unpaid debts. These can hurt your credit score. It also indicates a history of missed payments.

Account Status and History

It states information on how long your accounts have been open. This highlights your creditworthiness based on past behavior.

What Credit Bureaus Do Not Collect

While credit bureaus collect a lot of financial information. But, they do not include specific personal details, including:

Medical History

Your credit report does not include your health history. But unpaid medical bills or those sent to collections can appear.

Race, Ethnicity, and Religion

These factors are not part of your credit profile. Credit scoring should remain neutral and non-discriminatory.

Public Assistance or Government Benefits

Your credit report does not show your eligibility for or use of public assistance programs. But, debts related to such programs (like student loans) can.

Gender

Your credit profile also does not include your gender. It has no bearing on your ability to manage credit.

Personal Relationships

Credit bureaus do not record personal relationships unless they affect your ability to pay.

How Information Flows to and From Credit Bureaus

Credit bureaus collect and store information about your credit history from various sources. This includes banks, credit card companies, and lenders. These creditors report your credit activity to bureaus regularly. The information includes your payment history, credit utilization, and current debts. This data is then updated in your credit report. Credit bureaus can also share this information with lenders or other entities requesting it for lending decisions.

The Role of Creditors and Lenders in Reporting Your Credit Activity

Creditors provide regular updates on your credit activity to the credit bureaus. This includes whether you’ve made timely payments, credit limits, and other account details. This helps build your credit history.

Public Records and Utilities

Certain public records and utility companies can also contribute to your credit report. While utilities may not always report to credit bureaus, some do. Unpaid bills may end up on your report, affecting your credit score. Public records often show up as negative information.

How Your Credit Report Powers Lending Decisions and Credit Risk Assessments

Your credit report provides a detailed record of your credit history and behavior. Lenders use this information to assess your creditworthiness. They use it to check the risk of lending to you. They look at factors like your payment history and your credit utilization. This helps them decide whether to approve or deny your application, and what interest rate to offer.

Credit Bureaus vs. Credit Scoring Models

Credit bureaus are agencies that collect and maintain your credit data. They gather your credit history and compile it into a report. Meanwhile, credit scoring models like FICO Scores and VantageScore use the information from your credit report to calculate a numerical score. The score reflects your creditworthiness. While credit bureaus store your data, credit scoring models check it to provide a quick way for lenders to gauge your credit risk.

Why Your 3 Credit Reports May Not Be Identical

Here’s a breakdown of why your three credit reports may not be identical:

Variances in Reporting

Each of the three major credit bureaus may receive different information from creditors and lenders. This happens because not all lenders report to every bureau. Some may only report to one or two of them. As a result, your credit history may be different across the bureaus. This leads to discrepancies in your credit reports.

Differences in Reporting Cycles and Credit Report Updated Frequencies

The timing of credit report updating can vary between the bureaus. Lenders report your credit activity per month. But, they may report to the bureaus at different times during the month. Each bureau may have different versions of your credit history depending on when it received the most recent data.

The Impact of Discrepancies on Your Credit Scores and Loan Rates

Since each credit bureau may have a different version of your credit report, your credit score can vary from one bureau to another. Even slight differences can affect your credit score. This impacts lending decisions and loan rates.

The Strategic Importance of a 3-Bureau Credit Report for Comprehensive Review

Reviewing your credit reports from all three bureaus is crucial to understanding your credit health. A three-bureau credit report helps you identify discrepancies, errors, or missing information. It also lets you see how lenders and creditors report your data across different bureaus.

Building and Maintaining a Strong Credit Profile

Building and maintaining a strong credit profile involves managing your credit. This includes paying bills on time and keeping credit utilization low. It also includes ensuring your credit report remains accurate. A strong credit profile makes getting loan and credit card approvals easier.

Good Credit Habits

Good credit habits are essential for building and maintaining a strong credit profile. These include paying on time, avoiding high credit utilization, and reviewing your credit reports. These habits help establish a reliable credit history that lenders trust.

Credit Mix

Credit mix refers to the variety of credit accounts you have. A diverse credit mix shows lenders that you can handle different types of credit. But it’s not necessary to have every kind of credit. A healthy balance of other accounts is enough.

Authorized User Tradelines

Authorized user tradelines involve becoming an authorized user of someone else’s credit account. This allows you to inherit the account holder’s positive credit history. As a result, boost your credit score. It’s an effective way for someone with little or no credit history to improve their score.

One popular way to enjoy tradelines is by purchasing them from reliable tradeline companies. Coast Tradelines is one reliable name in this industry. Buying tradelines from Coast Tradelines means purchasing the opportunity to become an authorized user on a credit card with a positive history. This can give a quick boost to your credit score in a short time. Call us today if you’re interested.